On this page

IPO readiness is not an abstraction. It is the distance between what your finance function produces today and what an S-1 (or F-1, for foreign private issuers) requires on the day you file: PCAOB-audited financial statements, documented technical positions, a control environment, a tax provision, and a close process that can sustain quarterly reporting afterward. Companies that measure that distance early choose their timeline; companies that discover it late have their timeline chosen for them.

We structure readiness engagements around the gaps below, in the order auditors and the SEC will test them. Each section states what the requirement actually is, then the fix. If you want a fast read on where you stand, the free readiness assessment further down scores all of these in about fifteen minutes.

Financial statements built to what the S-1 requiresS-1 / Reg S-X

The S-1’s financial statement requirements are specific, and private-company financials almost never meet them as-is: the periods, the audit standard, the footnotes, and the interim stubs all change. This gap is the long pole in nearly every IPO timeline.

The fixThe S-1 requires audited annual financial statements, two years for emerging growth companies and three otherwise, audited under PCAOB standards by a registered firm, which usually means re-audit or uplift of existing AICPA audits. Add unaudited interim statements for the required stub periods, kept inside the staleness windows, full public-company footnotes (EPS, segments, fair value, equity, and the rest), and Regulation S-X compliant schedules. Foreign private issuers file the F-1 with IFRS as issued by the IASB, or local GAAP reconciled to US GAAP. The fix is sequencing: lock the required periods off your target filing date, start the PCAOB audit uplift immediately because it gates everything, and build the footnotes alongside the audit instead of after it. We prepare the statements, footnotes, and support so the auditors test rather than construct.

How we fix it: We prepare the S-1 financial statements, footnotes, and schedules, and manage the PCAOB audit uplift that gates the filing.

From our engagements: The most common surprise in readiness assessments: an existing clean audit that cannot support the S-1 because it was not performed under PCAOB standards. Finding that in month one instead of month nine is worth the assessment by itself.

Technical accounting positions documented before they are questionedASC 606 / 718 / 480

Revenue recognition, equity and convertible instruments, stock compensation, and unusual transactions drive most SEC comments and most pre-IPO restatements. Undocumented positions do not fail because they are wrong; they fail because nobody can show the analysis.

The fixInventory the judgment areas and write the position memos before the audit: ASC 606 revenue policies matched to how contracts actually work, SAFEs, converts, warrants, and preferred stock classified under ASC 480 and 815, ASC 718 stock compensation with the cheap stock bridge to the expected offering price, plus any business combinations, consolidation questions, or industry-specific issues. Each memo runs facts, guidance, alternatives, conclusion, and disclosure impact, in the format auditors and, later, SEC reviewers expect to test. The S-1’s MD&A critical accounting estimates section is then written from the memos, so the filing and the workpapers say the same thing.

How we fix it: We inventory the judgment areas and deliver the position memos before the audit, then write the critical estimates disclosure from them.

Gap 03

A control environment scaled to your listing timelineSOX

Undocumented controls will not block your S-1, but they will surface fast afterward: 302 certifications start with your first periodic report, management’s 404(a) assessment follows, and material weaknesses disclosed in the S-1 itself are now common and priced by investors.

The fixBuild the control environment to the actual regulatory sequence rather than all at once: entity-level and close controls first (they support the 302 certifications you sign immediately), then documentation of key cycles under COSO, then the testing program that management’s first 404(a) assessment requires, generally with your second annual report. Emerging growth companies get relief from auditor attestation under 404(b) for up to five years, which changes the investment curve but not the need for a reliable close. If a material weakness exists at filing, disclose it with a credible remediation plan; the disclosure is survivable, an undisclosed weakness discovered later is not. We design the framework a lean team can actually operate, sequenced to your dates.

How we fix it: We build the control framework in regulatory sequence: certification-critical controls first, then cycles, then the testing program.

Want to know which of these gaps you have? Start with the free assessment below, or talk to us directly.

Talk to an Expert

Gap 04

Tax provision and structure ready for public scrutinyASC 740

Many private companies have never prepared a full ASC 740 provision, and the S-1 requires one for every audited period: deferred taxes, valuation allowances, uncertain positions, and the rate reconciliation, plus a structure that survives diligence.

The fixBuild the provision history the filing needs: current and deferred taxes for each presented period, valuation allowance analysis with the positive and negative evidence documented (most pre-profit issuers carry full allowances, and the release timing later becomes its own judgment), uncertain tax position inventory, and state and foreign footprints reconciled. Structural items surface here too: Up-C structures and tax receivable agreements, Section 382 limitations on NOLs after funding rounds, and equity compensation deductions. The provision workpapers become audit support and the tax footnote simultaneously. Start this workstream early; rebuilding three years of provisions is slow, and it sits directly on the audit path.

How we fix it: We build the ASC 740 provisions for every presented period and the valuation allowance and structure analysis behind them.

Gap 05

Governance, audit committee, and the disclosure apparatusListing standards

Exchange listing standards and SEC rules require governance most private companies have not built: an audit committee with independence and financial expertise, formal policies, and a disclosure process that can stand behind certifications every quarter.

The fixStand up the pieces on the exchange’s phase-in schedule: an audit committee meeting independence requirements with at least one financial expert (fully independent within a year of listing), a disclosure committee and sub-certification process feeding the 302 certifications, and the policy set: related party transactions, whistleblower, insider trading with 10b5-1 awareness, and a Reg FD posture before the roadshow. The audit committee also formally owns the auditor relationship, so its charter and calendar need to exist before effectiveness, not after. We support the finance side of this: the reporting the committee reviews, the sub-certification design, and the related-party inventory the S-1 will disclose.

How we fix it: We support the finance side of governance: audit committee reporting, sub-certification design, and the related-party inventory the S-1 discloses.

Gap 06

The close process and team that quarterly reporting demandsOperations

A public company closes and files on statutory deadlines every quarter, forever. A close that takes six weeks, key-person spreadsheets, and systems that cannot produce footnote support are readiness gaps as real as any accounting position, and they surface in the first 10-Q.

The fixCompress and harden the close: a documented close calendar with owners targeting a timeline that supports the 10-Q deadline with review and auditor time built in, reconciliations standardized, footnote support (EPS, equity rollforwards, segment data, fair value tables) produced by the process rather than assembled after it, and the reporting calendar for the first four quarters mapped before pricing. Staff honestly: most issuers add SEC reporting capability, by hire or by outsourcing, before filing. This is also where the S-1 workload and the ongoing business collide, so plan the team for both. We frequently run the close and reporting alongside the readiness workstream so the internal team is not doing two jobs.

How we fix it: We compress the close, build the footnote support into the process, and can run reporting alongside your team so the S-1 does not stall the business.

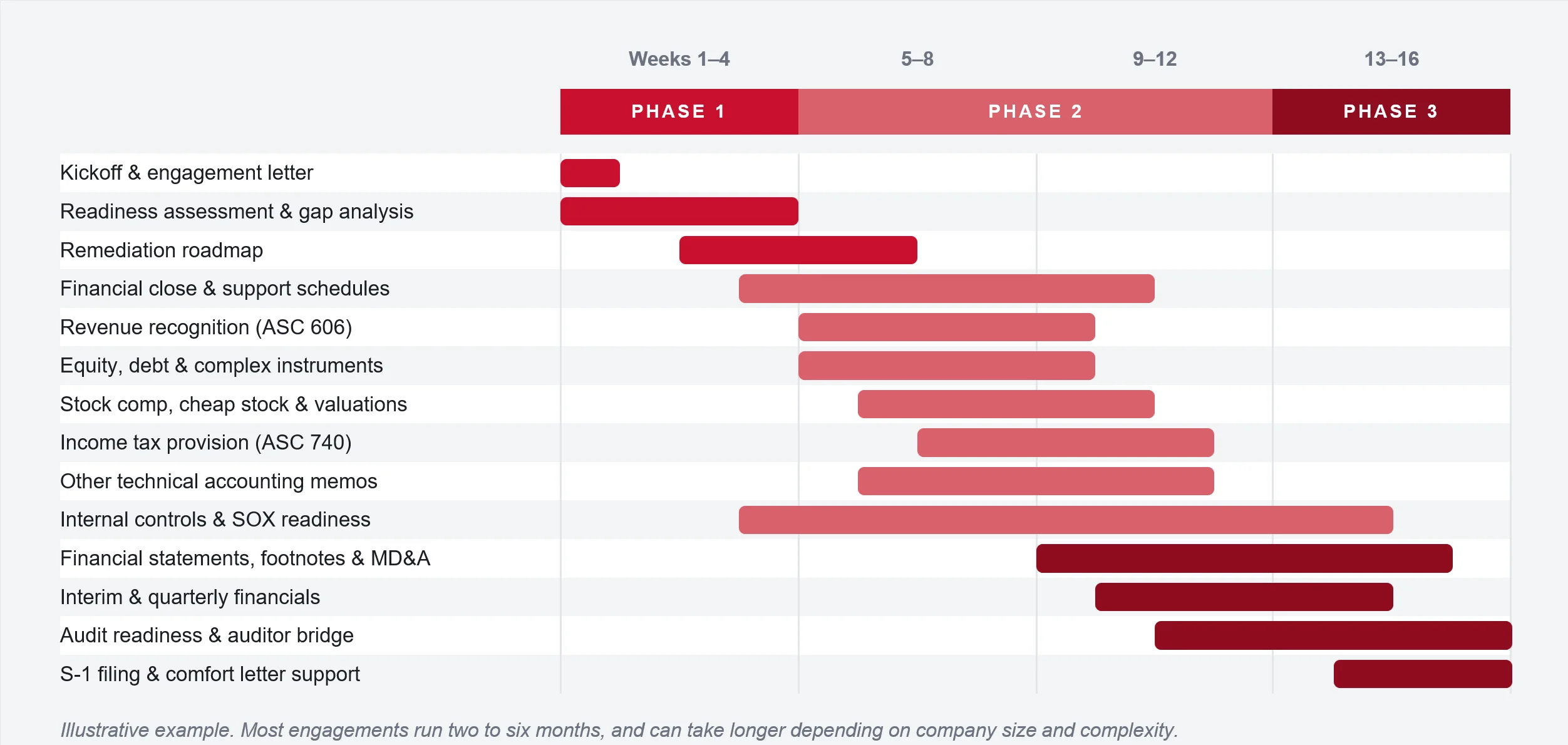

From our engagements: In our sixteen-week reference timeline, the close process work starts in week one, not at the end, because every later workstream, audit, stubs, comfort letters, consumes closes as raw material.